Watching the Economy by Clint Burdett CMC® FIMC

September 25, 2013

This

updates my October 8, 2012 article.

A key driver of consumer demand, our confidence we can spend more, is recovering from the Great Recession

and we are paid more -- pay cuts restored, new or better job, clients come back.

A concern this time is a

structural change in the labor market, older workers not finding jobs, which Josh Lerner for Oregon's Office

of Economic Analysis examines here.

The fact that there remains a large pool of the long-term unemployed can explain the

majority of the outward shift the Beveridge Curve [being used to compare younger to older workers unemployment]

and if there is a structural problem in the labor market, it is with these individuals who have been out

of work a long time. This is worrisome because to the extent that the skills of displaced

workers have become obsolete, permanent damage has been done to Oregon’s

growth potential. Ensuring that individuals who have been out of work for an extended period of time

remain a part of the labor force, and do not see their skills and productivity erode, is a challenge. [my

emphasis added]

So far, more new jobs are going to younger workers at lower wages,

but in aggregate, more wages are available to spend. To grow at historical trends, the older workers

need jobs too, even a lower wages.

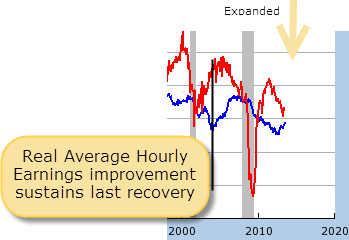

To observe the trend, we examine the relationship between national measures

of consumer pay and spending:

For pay, Real Average Hourly Earnings computed by the Bureau of Labor Statistics (BLS).

For spending, Real Personal Consumption Expenditures (PCE) computed by the Bureau of Economic Analysis (BEA) for consumer consumption of goods and services.

In both measures, real means inflation has been subtracted.

(Click to open on St Louis FRED)

Overtime, improved pay compared to a year ago leads to more consumption compared to a year ago, so average real

average hourly earnings improvement is usually a leading indicator for more household spending. Overtime, improved pay compared to a year ago leads to more consumption compared to a year ago, so average real

average hourly earnings improvement is usually a leading indicator for more household spending.

The Great Recession (or more accurately the Great Contraction) has not been a "normal" recession and the recovery will continue to be slow (Reinhart/Rogoff Oct 2012).

PCE compared to same time last year is declining.

You may not reprint this article for sale without my expressed written permission.

You may post or reprint this article to educate as long as you credit my work

and provide a link to www.clintburdett.com

|

|