Key Links Clint Follows | Clint's blog on economic trends

Best Source Aggregators with links to data

Calculated Risk

The best presentation and explanation of data using charts that I know of

Ahead of the Curve

Superb l/t analysis of business cycle, link to chart, leading indicator for increased consumer spending. Updated infrequently.

Census Bureau

Summary with links to charts, reports most recent at top, often with superb charts

NBER List of Upcoming Releases

National Bureau of Economic Research, they "call" the start and stop of a recession

Pending upcoming authorative reports with links

St Louis Federal Reserve - FRED data

Online charts you can define, use their templates or search for data series

Federal Reserve h.15 daily, weekly

Daily release, weekly summary for past week released on Monday yields

Key Economic Indicators

2Yr - 10Yr Treasury Constant Mature Yield Spread

2-10 spread, negative to positive for several months indicates recession likely in just over one year

(or 10-2 spread positive to negative)

Click to see larger image Click to see larger image

Inflation

Personal Consumption Expenditures and Core Personal Consumption Expenditures Exlcuding Food and Energy

PCEPI and PCEPILFE, the index of chained dollars -m

The Fed target is 2% for previous year to stimulate growth

Click to see larger image Click to see larger image

Consumer Spending

Clint's exploring Joseph H. Ellis's observation of rate of change compared to last year

Real PCE bottom to end of recession and USA Total Industrial Production (Ellis's Chart 7-3)

Here there is a remarkable consistency (correlation) between Real PCE and Total Industrial Production rate of growth peak and trough year on year. I am uncertain if PCE and Production are causative. I suspect earnings, population and other factors change spending patterns.

Click to see larger image Click to see larger image

PCE YoY % Change (PCECC96 by quarter since 1/1/1947 or PCEC96 monthly since 1/1/1999)

Personal Consumption Expenditures 2005 Chained Dollars -m

Generally, > 2.5% PCE increase from previous year sustains 3% or greater GDP growth

Click to go to StLouisFed FRED graph editor) Click to go to StLouisFed FRED graph editor)

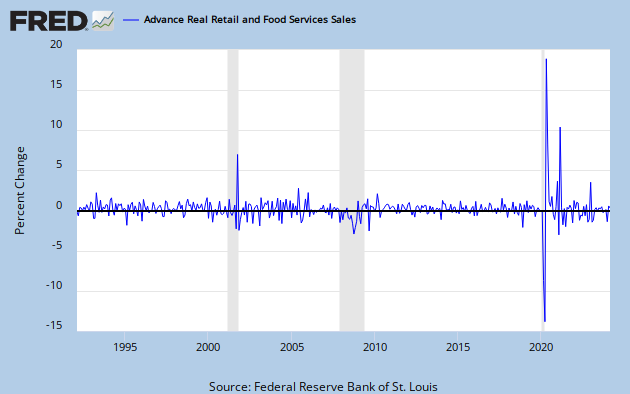

Retail Sales

Retail and Food Services Sales Change from Previous Month

% change month on month on real retail and food services sales. -abt12bd -m

Not seasonally adjusted. More positive change indicates growing economy.

Click to go to St Louis Fed FRED graph editor Click to go to St Louis Fed FRED graph editor

Clint's Version

Compares Retail Sales ex Gasoline to PCE (consumer spending) YoY rate of growth/decline using trailing 3 months for smoothing.

A rule of thumb is a change of direction over three months is significant.

Average line for last 24 months used to determine growth rate comparisons trending up, down or flat.

Click to see larger image Click to see larger image

Without smoothing, the movement is more dramatic, which is often called noise.

Click to see larger image Click to see larger image

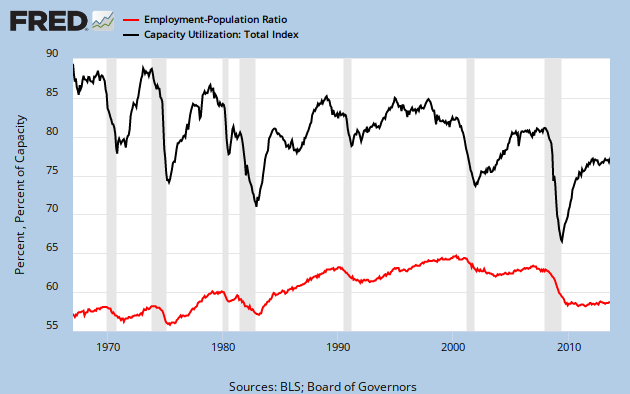

Unemployment to Total Capacity Utilization

St Louis Fred Total Capacity Utilization (TCU) and Percent of US Population Employed (EMRATIO)

Total Capacity Utilization -2m, Unemployed % of Total Population -1m

Long term trends on capacity and jobs growth or loss

Click to go to St Louis Fed FRED graph editor Click to go to St Louis Fed FRED graph editor

Clint's Observation

In the recoveries for the 2002 recession and the 2008 Great Recession, the percentage of US population stays flat. Hiring does not exceed normal population growth.

Click to see larger image Click to see larger image

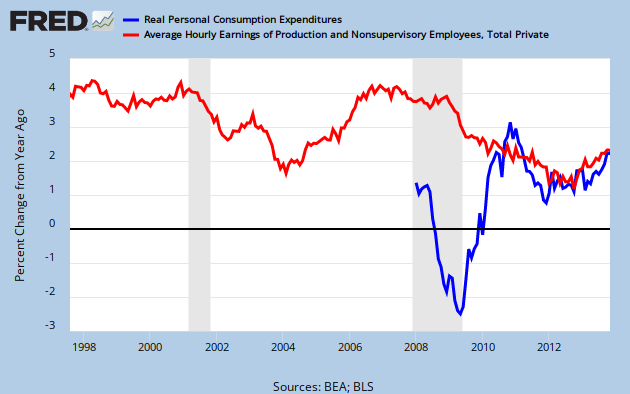

Earnings

Real PCE Rate of Change YoY to Private Industry Hourly Earnings YoY Rate of Change

Historically, downward change in an individual's real average hourly earnings a leading indicator (12 m or more) lead to PCE decline

(see AheadoftheCurve-thebook.com)

Click to go to St Louis FED FRED graph editor Click to go to St Louis FED FRED graph editor

Clint's Observation

Total nonfarm employees times average hourly earnings equals total income. More hiring, flat wages, less income than more hiring, rising wages.

Click to see larger image Click to see larger image

Credit and Liquidity -- reported daily

LIBOR US Over Night

London Interbank Offered Rate from British Banking Association

Overnight cost of borrowing in USD. Moves up, credit tightening.

Click to go to St Louis Fed FRED graph editor Click to go to St Louis Fed FRED graph editor

Ted Spread 3 month

Treasury-bill to Euro Dollar spread in bps. Spread widening, liquidity being withdrawn.

Click to go to St Louis Fed graph editor Click to go to St Louis Fed graph editor

LIBOR US 3 month term

London Interbank Offered Rate

Interest rate for bank unsecured loans. Moving up, credit tightening.

Click to go to St Louis Fed FRED graph editor Click to go to St Louis Fed FRED graph editor

VIX (real time on Bloomberg)

Chicago Board Options Exchange Volatility Index, implied volatility in S&P 500 index options next 30 days.

Moving up, options cost more, investors expect market to be more volatile.

Click to go to St Louis Fed FRED graph editor Click to go to St Louis Fed FRED graph editor

2YR USD Swap Spread (adjust chart period to 5 years)

The spread between the rate to exchange floating currency fixed interest payments and Treasury yields for two years notes.

A SWAP is a form of insurance, in the event the underlying securities will not make payments, the seller of the swap pays the interest and receives the underlying security. The spread is the relative "cost" of the insurance.

Housing -- for last month or quarter

Privately Owned Permits, Housing Starts, Months of Supply

Issued last Wednesday of the month for previous month

In this chart, months of supply is inverted and leads the issue of permits or start of construction

") Click to see larger image Click to see larger image

Delinquent +30 +60 +90 days

past due % of all loans

Issued in Mar, Jun, Sep, & Dec on 5th Business Day for previous quarter's data

At least two months time late.

Foreclosures % of loans

At least, two months time late

Issued in Mar, Jun, Sep, & Dec on 5th Business Day for previous quarter's data

New Home Sales

Annual pace of sales from Census & HUD

(SAAR seasonal adjusted annual rate 000)

Issued 4th Wednesday for previous month's data

For new construction reported upon a deposit at any stage of construction.

Months Supply Supply New Homes

See 1st page of Census press release in PDF

Pending Home Sales

MoM (month on month) % change pending home sale index

Issued 4th Wednesday for previous month's data

Contract signed to buy previously owned home, waiting on escrow about 2 months out. Similar to New Home Sales after deposit.

Existing Home Sales

Annual pace of sales (SAAR 000,000)

Issued 4th Wednesday for previous month's data

Report after closing escrow.

Months Supply Existing Homes

Months of supply of existing homes.

Issued 3rd Thursday for previous month's data

Normal is about 7 months or less.

National Association of Home Builders (NAHB) Housing Contribution to GDP

Breakout of GDP from private investment (new homes) and housing services from BEA GDP data

One quarter in the past

Since 1970 -2009 averaging 18.1%, last 6 quarters through 13Q1 15.1%

|